Investing Education

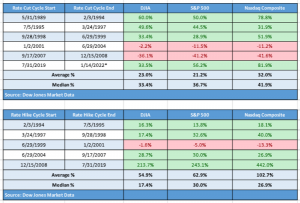

Market Performance During Rate Increases & Decreases Since 1989

What is a 401(k) Plan?

A 401(k) plan is a retirement savings plan offered by many American employers that has tax advantages to the saver. It is named after a section of the U.S. Internal Revenue Code.

The employee who signs up for a 401(k) agrees to have a percentage of each paycheck paid directly into an investment account. The employer may match part or all of that contribution. The employee gets to choose among a number of investment options, usually mutual funds.

KEY TAKEAWAYS

- A 401(k) plan is a company-sponsored retirement account that employees can contribute income, while employers may match contributions.

- There are two basic types of 401(k)s—traditional and Roth—which differ primarily in how they’re taxed.

- With a traditional 401(k), employee contributions are “pre-tax,” meaning they reduce taxable income, but withdrawals are taxed.

- Employee contributions to Roth 401(k)s are made with after-tax income; there’s no tax deduction in the contribution year, but withdrawals are tax-free.

How 401(k) Plans Work

The 401(k) plan was designed by the United States Congress to encourage Americans to save for retirement. Among the benefits they offer is tax savings.

There are two main options, each with distinct tax advantages:

Traditional 401(k)

With a traditional 401(k), employee contributions are deducted from gross income, meaning the money comes from the employee’s payroll before income taxes have been deducted.

As a result, the employee’s taxable income is reduced by the total amount of contributions for the year and can be reported as a tax deduction for that tax year. No taxes are due on the money contributed or the earnings until the employee withdraws the money, usually in retirement.

Roth 401(k)

With a Roth 401(k), contributions are deducted from the employee’s after-tax income, meaning contributions come from the employee’s pay after income taxes have been deducted. As a result, there is no tax deduction in the year of the contribution.

When the money is withdrawn during retirement, no additional taxes are due on the employee’s contribution or the investment earnings.

However, not all employers offer the option of a Roth account. If the Roth is offered, the employee can pick one or the other or a mix of both, up to annual limits on their tax-deductible contributions.

Contributing to a 401(k) Plan

A 401(k) is a defined contribution plan. The employee and employer can make contributions to the account up to the dollar limits set by the Internal Revenue Service (IRS).

A defined contribution plan is an alternative to the traditional pension, known in IRS lingo as a defined-benefit plan. With a pension, the employer is committed to providing a specific amount of money to the employee for life during retirement.

In recent decades, 401(k) plans have become more common, and traditional pensions have become rare as employers shifted the responsibility and risk of saving for retirement to their employees.

Employees also are responsible for choosing the specific investments within their 401(k) accounts from a selection their employer offers. Those offerings typically include an assortment of stock and bond mutual funds and target-date funds designed to reduce the risk of investment losses as the employee approaches retirement.

They may also include guaranteed investment contracts (GICs) issued by insurance companies and sometimes the employer’s own stock.

Contribution Limits

The maximum amount that an employee or employer can contribute to a 401(k) plan is adjusted periodically to account for inflation, which is a metric that measures rising prices in an economy.

For 2024, the annual limit on employee contributions is $23,000 per year for workers under age 50, the limit is $30,500 per year if you are over 50 years old.

If the employer also contributes, or if the employee elects to make additional, non-deductible after-tax contributions to their traditional 401(k) account, there is a total employee-and-employer contribution amount for the year.

2024

- For workers under 50 years old, the total employee-and-employer contribution amount is capped at $69,000, or 100% of employee compensation, whichever is lower.

- If we include the catch-up contribution for those 50 and over, the limit is $76,500.

Employer Matching

Employers who match their employee contributions use various formulas to calculate that match.

For instance, an employer might match 50 cents for every dollar the employee contributes up to a certain percentage of salary.

Financial advisors often recommend that employees contribute at least enough money to their 401(k) plans to get the full employer match.

Contributing to Both a Traditional and Roth 401(k)

If their employer offers both types of 401(k) plans, employees can split their contributions, putting some money into a traditional 401(k) and some into a Roth 401(k).

However, their total contribution to the two types of accounts can’t exceed the limit for one account (such as $23,000 for those under age 50 in 2024, & $30,500 if over 50 years old).

Employer contributions can only go into a Traditional 401(k) account where they will be subject to tax upon withdrawal, not into a Roth.

Taking Withdrawals From a 401(k)

Once money goes into a 401(k), it is difficult to withdraw it without paying taxes on the withdrawal amounts.

The earnings in a 401(k) account are tax-deferred in the case of traditional 401(k)s and tax-free in the case of Roth IRAs. When the traditional 401(k) owner makes withdrawals, that money (which has never been taxed) will be taxed as ordinary income.

Roth account owners have already paid income tax on the money they contributed to the plan and will owe no tax on their withdrawals as long as they satisfy certain requirements.

Both traditional and Roth 401(k) owners must be at least age 59½—or meet other criteria spelled out by the IRS, such as being totally and permanently disabled—when they start to make withdrawals.

Otherwise, they usually will face an additional 10% early-distribution penalty tax on top of any other tax they owe.

Some employers allow employees to take out a loan against their contributions to a 401(k) plan. The employee is essentially borrowing from themselves.

If you take out a 401(k) loan, please consider that if you leave the job before the loan is repaid, you’ll have to repay it in a lump sum or face the 10% penalty for an early withdrawal.

Required Minimum Distributions

Traditional 401(k) account holders are subject to required minimum distributions, or RMDs, after reaching a certain age. (Withdrawals are often referred to as “distributions” in IRS parlance.)

After age 72, account owners who have retired must withdraw at least a specified percentage from their 401(k) plans, using IRS tables based on their life expectancy at the time. (Prior to 2020, the RMD age was 70½ years old.)

Note that distributions from a traditional 401(k) are taxable. Qualified withdrawals from a Roth 401(k) are not.

Roth IRAs, unlike Roth 401(k)s, are not subject to RMDs during the owner’s lifetime.

Traditional 401(k) vs. Roth 401(k)

When 401(k) plans became available in 1978, companies and their employees had just one choice: the traditional 401(k). Then, in 2006, Roth 401(k)s arrived. Roth accounts are named for former U.S. Senator William Roth of Delaware, the primary sponsor of the 1997 legislation that made the Roth IRA possible.

While Roth 401(k)s were a little slow to catch on, many employers now offer them. So the first decision employees often have to make is between Roth and traditional.

As a general rule, employees who expect to be in a lower marginal tax bracket after they retire might want to opt for a traditional 401(k) and take advantage of the immediate tax break.

On the other hand, employees who expect to be in a higher bracket after retiring might opt for the Roth so that they can avoid taxes on their savings later. Also important—especially if the Roth has years to grow—is that there is no tax on withdrawals, which means that all the money the contributions earn over decades of being in the account is tax-free.

As a practical matter, the Roth reduces your immediate spending power more than a traditional 401(k) plan. That matters if your budget is tight.

Since no one can predict what tax rates will be decades from now, neither type of 401(k) is a sure thing. For that reason, many financial advisors suggest that people hedge their bets, putting some of their money into each.

When You Leave Your Job

When an employee leaves a company where they have a 401(k) plan, they generally have four options:

1. Withdraw the Money

Withdrawing the money is usually a bad idea unless the employee urgently needs the cash. The money will be taxable in the year it’s withdrawn. The employee will be hit with the additional 10% early distribution tax unless they are over 59½, permanently disabled, or meet the other IRS criteria for an exception to the rule.

This rule was suspended for 2020 for those affected by the 2020 COVID-19 economic crisis.

In the case of Roth IRAs, the employee’s contributions (but not any profits) may be withdrawn tax-free and without penalty at any time as long as the employee has had the account for at least five years. Remember, they’re still diminishing their retirement savings, which they may regret later.

2. Roll Your 401(k) Into an IRA

By moving the money into an IRA at a brokerage firm, a mutual fund company, or a bank, the employee can avoid immediate taxes and maintain the account’s tax-advantaged status. What’s more, the employee will be able to choose among a wider range of investment choices than with their employer’s plan.

The IRS has relatively strict rules on rollovers and how they need to be accomplished, and running afoul of them is costly. Typically, the financial institution that is in line to receive the money will be more than happy to help with the process and avoid any missteps.

Funds withdrawn from your 401(k) must be rolled over to another retirement account within 60 days to avoid taxes and penalties.

3. Leave Your 401(k) With the Old Employer

In many cases, employers will permit a departing employee to keep a 401(k) account in their old plan indefinitely, although the employee can’t make any further contributions to it.

This generally applies to accounts worth at least $5,000. In the case of smaller accounts, the employer may give the employee no choice but to move the money elsewhere.

Leaving 401(k) money where it is can make sense if the old employer’s plan is well managed and the employee is satisfied with the investment choices it offers. The danger is that employees who change jobs over the course of their careers can leave a trail of old 401(k) plans and may forget about one or more of them.

Their heirs might also be unaware of the existence of the accounts.

4. Move Your 401(k) to a New Employer

You can usually move your 401(k) balance to your new employer’s plan. As with an IRA rollover, this maintains the account’s tax-deferred status and avoids immediate taxes.

It could be a wise move if the employee isn’t comfortable with making the investment decisions involved in managing a rollover IRA and would rather leave some of that work to the new plans administrator.

Source: Investopedia

Top Reasons to Roll Over Your 401(k) to an IRA

When you change jobs, you usually have four options for your 401(k) plan account. You can cash it out (and pay taxes), leave it where it is (if your ex-employer allows this), transfer it into your new employer’s 401(k) plan (if one exists), or roll it over into an individual retirement account (IRA).

For most people, rolling over a 401(k) (or its 403(b) cousin for those in the public or nonprofit sector) is the best choice. This article explains why and how to go about it.

KEY TAKEAWAYS

- When you change jobs, you have several options for what to do with the 401(k) plan at your old employer.

- For many people, rolling their 401(k) account balance over into an IRA is the best choice.

- By rolling your 401(k) money into an IRA, you’ll avoid immediate taxes and your retirement savings will continue to grow tax-deferred.

- An IRA may also offer you more investment choices and greater control than your old 401(k) plan did.

1. More Investment Choices

Your 401(k) is limited to a few planets in the investment universe. In all likelihood, you have a choice of mutual funds from one particular provider. However, with an IRA, you can invest just about anywhere.

In addition, you’re likely to have more types of investments to choose from—not just mutual funds but also individual stocks, bonds, and exchange-traded funds (ETFs), to name a few.

IRAs open a larger universe of investment choices. Most 401(k) plans do not allow the use of risk management, such as options, but IRAs do. It is even possible to hold income-producing real estate in your IRA.

You can also buy and sell holdings any time you want. Most 401(k) plans limit the number of times per year that you can rebalance your portfolio, as the pros put it, or restrict you to certain times of the year.

2. Better Communication

If you leave your account with your old employer, you might be treated as a second-class citizen, though not deliberately. It just could be harder to get communications regarding the plan (often news is distributed through company email) or to get in touch with an advisor or administrator.

Having ready access to information is extra important in the unlikely event something goes south at your old workplace. You don’t want your former employer to file bankruptcy and your money is affected.

3. Lower Fees and Costs

Rolling your money over into an IRA will often reduce the management and administrative fees you’ve been paying, which can eat into your investment returns over time. The funds offered by the 401(k) plan may be more expensive than the norm for their asset class.

And on top of that, there is the overall annual fee that the financial institution managing the plan charges.

Investors should be careful about the transaction costs associated with buying certain investments and the expense ratios, 12b-1 fees, or loads associated with mutual funds. All of these can easily be more than 1% of total assets per year.

Admittedly, the opposite can also be true. The bigger 401(k) plans with millions to invest have access to institutional-class funds that charge lower fees than their retail counterparts. Of course, your IRA won’t be free of fees either.

But again, you’ll have more choices and more control over how you’ll invest, where you’ll invest, and what you’ll pay.

4. The Option to Convert to a Roth

An IRA rollover opens up the possibility of switching to a Roth account. (In fact, if yours is one of the increasingly common Roth 401(k)s, a Roth IRA is the preferred rollover option.)

With Roth IRAs, you pay taxes on the money you contribute when you contribute it, but there is no tax due when you withdraw money, which is the opposite of a traditional IRA. Nor do you have to take required minimum distributions (RMDs) at age 73 or ever from a Roth IRA.

If you believe that you will be in a higher tax bracket or that tax rates will be generally higher when you start needing your IRA money, switching to a Roth—and taking the tax hit now—might be in your best interest.

If you’re under the age of 59½, it’s also a lot easier to withdraw funds from a Roth IRA than from a traditional one. In most cases, there are no early withdrawal penalties for your contributions, but there are penalties if you take out any investment earnings.

Your 401(k) plan rules may only permit rollovers to a traditional IRA. If so, you’ll have to do that first and then convert the traditional IRA into a Roth. There are a number of strategies for when and how to convert your traditional IRA to a Roth that can minimize your tax burden.

Should the market experience a significant downturn, converting a traditional IRA that is down, say 20% or more, to a Roth will result in less tax due at the time of the conversion. If you plan to hold the investments until they recover, that could be an attractive strategy.

But this can be tricky, so if a serious amount of money is involved, it’s probably best to consult with a financial advisor to weigh your options.

5. Cash or Other Incentives

Financial institutions are eager for your business. To entice you to bring them your retirement money, they may throw some cash your way. In late 2021, for example, TD Ameritrade was offering bonuses of up to $2,500 when you rolled over your 401(k) into one of its IRAs. If it’s not cash, free stock trades can be part of the package at some companies.

6. Fewer (and Clearer) Rules

Understanding your 401(k)’s rules can be no easy task because employers have a lot of leeway in how they set up their plans. In contrast, IRA regulations are standardized by the Internal Revenue Service (IRS). An IRA at one financial institution follows substantially the same rules as one at any other.

An often-overlooked difference between a 401(k) and an IRA has to do with IRS rules regarding taxes on distributions. The IRS requires that 20% of distributions from a 401(k) be withheld for federal taxes. When you take a distribution from an IRA, you can elect to have no tax withheld.

It’s probably wise to have some tax withheld rather than winding up with a big tax bill at the end of the year and possibly owing interest and penalties for underpayment. However, you can choose how much to have withheld to more accurately reflect the actual amount you’ll owe, rather than an automatic 20%.

The benefit is that you’re not depleting your retirement account faster than you need to, and you’re allowing that money to continue compounding on a tax-deferred basis.

7. Estate Planning Advantages

Upon your death, there’s a good chance that your 401(k) will be paid in one lump sum to your beneficiary, which could cause income and inheritance tax headaches. Rules vary depending on the particular plan, but most companies prefer to distribute the cash quickly so they don’t have to maintain the account of an employee who is no longer there.

Inheriting an IRA has tax implications too, but IRAs offer more payout options.

How to Roll Over Your 401(k) to an IRA

The easiest and safest way to roll over your 401(k) into an IRA is with a direct rollover from the financial institution that manages your 401(k) plan to the one that will be holding your IRA. (It might even be the same financial institution if you like its IRA offerings.)

Your plan administrator can guide you through the process, and the financial institution where your money is going will usually be more than happy to assist. In many cases, your plan administrator will give you a check made out to your new IRA custodian for you to deposit there.

Another option—but a far riskier one—is to have the check made out to you and take possession of the money yourself. If you do that, you typically have just 60 days from the date you received it to roll it over into an IRA.

If you fail to meet that deadline, the distribution will be treated as a withdrawal, and you’ll be subject to income taxes and possibly penalties on the full amount.

A further complication of receiving the distribution yourself is that your ex-employer will be required to withhold 20% of it for taxes. If you then want to deposit your full balance into an IRA, you’ll have to come up with other money to make up for the 20% that’s been withheld.

Can You Roll Over an IRA Into a 401(k)?

Yes, if your 401(k) plan permits it, you can roll over a traditional IRA (but not a Roth IRA) into it. Sometimes referred to as a reverse rollover.

What Happens If I Cash Out My 401(k)?

If you simply cash out your 401(k) account, you’ll owe income tax on the money. In addition, you’ll generally owe a 10% early withdrawal penalty if you’re under the age of 59½. It is possible to avoid the penalty, however, if you qualify for one of the exceptions that the IRS lists on its website.

Those include using the money for qualified education expenses or up to $10,000 to buy a first home.

What Are the Advantages of Leaving My 401(k) With My Ex-Employer

You might consider leaving your 401(k) with your ex-employer if you believe the plan is well run, its expenses are reasonable, and you don’t want the responsibility of managing the money yourself.

However, make sure you don’t lose track of the account over the years and that the plan administrator always has your current address.

Note also that this doesn’t have to be an all-or-nothing decision. You may be able to keep some of your balance in your old 401(k) and roll the rest into an IRA. After that, you can contribute to both your new company’s 401(k) and your IRA as long as you don’t go over the annual contribution limits.

The Bottom Line – For most people switching jobs, there are many advantages to rolling over their 401(k) into an IRA. But shop around for an IRA provider with low expenses. That can make a big difference in how much money you’ll have at your disposal when you retire.

Source: Investopedia